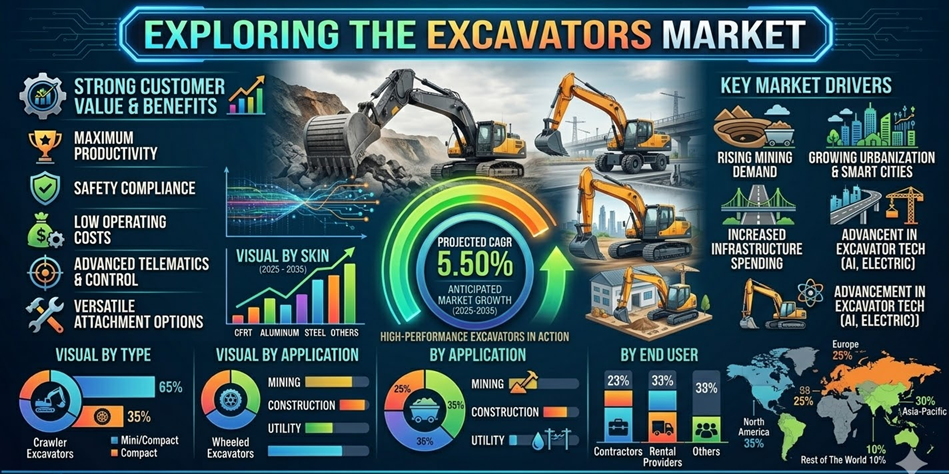

According to a comprehensive analysis by Market Research Future, the global Excavators Market was valued at USD 74.5 billion in 2024 and is projected to grow from USD 78.6 billion in 2025 to USD 134.3 billion by 2035, at a compound annual growth rate (CAGR) of 5.50% throughout the forecast period. This near-doubling of market value across a decade — in a market already measured in the tens of billions — reflects the structural depth and breadth of global excavator demand, and the extraordinary technological transformation that is simultaneously expanding the excavator’s capabilities and reshaping the competitive dynamics of the entire industry.

What Is an Excavator and Why Is It Central to Global Construction?

The hydraulic excavator as we know it today — with its characteristic articulated boom-and-arm digging mechanism, rotating upper structure (or “house”), and crawler or wheeled undercarriage — evolved from mechanical cable-operated shovels through a series of hydraulic technology advances during the 1960s and 1970s that replaced cable and lever actuation with the precise, powerful, and infinitely controllable hydraulic cylinder systems that define modern excavator operation. The result was a machine of extraordinary versatility: by swapping the standard bucket for any of dozens of specialized attachments — hydraulic hammers, grapples, thumbs, shears, tilting buckets, augers, compactors, rippers, and more — a single excavator platform can perform foundation digging, demolition, rock breaking, material handling, pipe laying, land clearing, slope stabilization, ditch maintenance, and dozens of other tasks on a single jobsite, often without leaving the operator’s cab.

This attachment versatility, combined with the crawler excavator’s ability to operate on unstable ground and slope gradients that would immobilize wheeled equipment, makes excavators the first machine deployed on most construction and civil engineering projects and often the last to leave — performing site preparation, structural excavation, underground utilities installation, landscape grading, and final cleanup operations across the full project lifecycle.

The excavator market is broadly divided into two major machine categories. Mini and compact excavators — typically defined as machines in the 0.8–6 metric ton operating weight range — are optimized for urban and confined-space applications where their minimal footprint, zero-tail-swing designs, and ability to work in proximity to existing structures make them invaluable for utility work, landscaping, residential construction, and indoor demolition. Standard and large excavators — ranging from 6 tons to over 800 tons in the largest mining models — serve the full spectrum of construction, civil engineering, and mining applications where digging depth, reach, bucket capacity, and force generation are the defining performance metrics.

Get An Exclusive Sample of the Research Report: https://www.marketresearchfuture.com/sample_request/2332

Key Market Drivers Accelerating Growth to 2035

Global Infrastructure Investment Wave: The single most powerful structural driver of excavator demand is the extraordinary scale of global infrastructure investment being committed across every major economy. The United States’ Infrastructure Investment and Jobs Act, the European Union’s REPowerEU and TEN-T network programs, China’s Belt and Road and domestic infrastructure stimulus programs, India’s National Infrastructure Pipeline (NaBFID’s USD 2.5 billion development finance mandate and the country’s real estate market projected to reach USD 1 trillion by 2030), Saudi Arabia’s Vision 2030 construction programs, and comparable investment waves across Southeast Asia, sub-Saharan Africa, and Latin America are collectively generating the most concentrated period of infrastructure construction in human history. Every kilometer of road, every bridge span, every railway cutting, every water treatment facility foundation, and every port expansion generates direct excavator demand — and the scale of committed infrastructure investment across the forecast period ensures that this demand pulse will sustain and grow throughout the decade to 2035.

Urbanization and the Construction Demand Multiplier: The global urban population is growing by approximately 68 million people per year, and every one of those people needs housing, water, sanitation, transportation, and public facilities — all of which require construction, and therefore excavators. The developing world’s urbanization is proceeding at the most rapid pace in Asia and Africa, where city populations are doubling over 15–20 year periods, generating construction demand at rates that significantly outpace the global average. India exemplifies this dynamic: its rapid urbanization, massive government infrastructure programs, and real estate market trajectory are driving excavator market growth at rates that make it the fastest-growing individual national market within the Asia-Pacific region. The construction sector’s projected CAGR of approximately 5.5% over the forecast period compounds directly into excavator demand growth.

Mining Sector Expansion and Critical Minerals: The excavator market’s mining application segment is identified as the fastest-growing among the three application categories, and the structural driver is unambiguous: the global energy transition requires enormous and rapidly growing quantities of copper, lithium, cobalt, nickel, manganese, rare earth elements, and other critical minerals that must be extracted from the earth at scales and rates significantly above current production. Every new mine development — from exploration bulk sampling through open-pit development, ore stripping, and waste rock management — requires excavators throughout its operational life. The mining segment was valued at USD 9.92 billion in 2024, and its growth trajectory reflects the extraordinary capital investment being made in global mining capacity to supply the battery, solar, wind, and grid infrastructure of the clean energy economy. Large hydraulic mining excavators — the 50–800 ton class — are among the highest-value individual machine transactions in the entire construction equipment industry, and the pipeline of new mine developments across Australia, Chile, the DRC, Indonesia, the Philippines, Canada, and elsewhere is generating growing order books for the largest excavator manufacturers.

The Electric and Hybrid Excavator Revolution: The most consequential technological transformation reshaping the excavator market is the rapid development and commercialization of electric and hybrid-electric excavator platforms. Driven by tightening emissions regulations (particularly Stage V and equivalent standards in Europe and Tier 4 Final in North America, with Stage 6 regulations emerging), urban jobsite noise and exhaust restrictions, and the operational economics of reduced fuel costs and lower maintenance complexity relative to diesel hydraulic systems, electric excavators are transitioning from experimental prototypes to commercially deployed equipment across a widening range of machine sizes. Volvo Construction Equipment’s comprehensive sustainability program — including its commitment to carbon neutrality by 2030 and its electric excavator product launches — and Komatsu’s hybrid excavator line launch reflect the strategic seriousness with which the industry’s leading manufacturers are approaching this technology transition. The market for electric excavators is expected to grow significantly through the forecast period, with the compact and mini excavator categories leading adoption (where battery weight-to-capacity ratios are most favorable and urban zero-emission zone requirements most frequently applicable) and larger machine electrification following as battery energy density and charging infrastructure improve.

Smart Technology Integration and Digitalization: Excavators are being transformed from mechanical-hydraulic machines into intelligent, connected, data-generating assets by the integration of telematics, machine control systems, automation technologies, and artificial intelligence. Caterpillar’s partnership with a leading technology firm to develop AI-driven excavators for enhanced operational efficiency and reduced fuel consumption, and Komatsu’s ICT-construction platform that uses GPS, machine control, and digital terrain modeling to guide operators with centimeter-level precision — both exemplify the industry’s accelerating investment in machine intelligence. Telematics systems that transmit real-time machine performance, location, fuel consumption, and fault data to fleet management platforms enable rental companies, contractors, and OEM service networks to optimize machine utilization, prevent unplanned downtime, and schedule predictive maintenance before failures occur. Semi-autonomous and fully autonomous excavator systems — enabling remotely operated machines on dangerous demolition, tunneling, and mining jobsites — are advancing from R&D programs toward commercial deployment at OEM production facilities and research-intensive mining operations. The integration of smart technology into excavators is not merely a feature upgrade; it is redefining the excavator’s role from a machine operated by a skilled individual to an intelligent asset managed within a connected construction digital ecosystem.

Buy this Premium Research Report: https://www.marketresearchfuture.com/checkout?currency=one_user-USD&report_id=2332

Government Initiatives and Public-Private Infrastructure Funding: Government infrastructure funding programs worldwide are providing the demand foundation that sustains excavator sales through cyclical economic fluctuations. India’s NaBFID establishment, the US Infrastructure Investment and Jobs Act, the EU’s structural and cohesion funds directed at transportation infrastructure, Saudi Arabia’s NEOM and Vision 2030 construction programs, and China’s periodic infrastructure stimulus packages all translate directly into contracted construction projects that require excavator fleet deployment. Public-private partnerships for infrastructure development — increasingly common across emerging markets where governments seek to leverage private capital alongside public funding — extend the reach of government infrastructure investment into project categories that would otherwise be beyond public sector funding capacity, multiplying the construction activity generated per unit of public budget commitment.

Market Segmentation Insights

By Type — Mini/Compact Leads, Crawler/Wheeled Grows: The mini and compact excavator segment holds the largest market share by unit volume, reflecting the enormous global installed base of small excavators serving urban utilities, residential construction, landscaping, and confined-space work across the developed and developing world alike. The mini excavator category’s growth is sustained by the continuing expansion of urban construction activity, the proliferation of utility network installation and repair work generated by aging infrastructure replacement programs, and the suitability of mini excavators for the rental business model. Crawler and wheeled excavators — the standard and large machine categories — are growing as the fastest segment by value, driven by the high average selling prices of larger machines and the expanding demand from infrastructure megaprojects, mining operations, and industrial construction that favor larger machine sizes for productivity efficiency.

By End User — Contractors Dominate, Rental Providers Accelerate: Contractors represent the dominant end-user category, projected to reach USD 42.5 billion by 2035, reflecting the fundamental role of excavators in construction project execution across residential, commercial, civil, and industrial project categories. Rental providers are the fastest-growing end-user segment — projected at USD 30.5 billion by 2035 — reflecting a structural industry trend toward equipment rental over ownership, driven by capital allocation efficiency, project-specific machine requirements, technology obsolescence risk management, and the growing sophistication of rental fleet management in emerging markets. The rental model’s growth is particularly pronounced in developing markets where contractor balance sheets cannot support large owned fleet investment, and in developed markets where the pace of technology change makes machine ownership less economically attractive than accessing the latest models through rental.

By Application — Construction Dominates, Mining Accelerates: Construction is the dominant application, valued at USD 29.88 billion in 2024 and projected to reach the largest absolute market position by 2035, anchored by the breadth and scale of global construction investment across residential, commercial, civil, and industrial project categories. Mining is the fastest-growing application, expanding from USD 9.92 billion in 2024 at rates substantially above the market average, driven by the critical minerals demand wave discussed above. The utility application — encompassing water and wastewater infrastructure, telecommunications cable installation, gas and electricity distribution network maintenance, and municipal services — contributes a stable and growing third leg of demand that benefits from the global program of aging infrastructure renewal across developed economies.

Regional Market Dynamics

Asia-Pacific is both the world’s largest regional market (USD 20.7 billion in 2022 and growing rapidly) and its fastest-growing, driven by the extraordinary concentration of infrastructure investment, urbanization, and industrialization across China, India, South Korea, Japan, Vietnam, Indonesia, and the broader Southeast Asian development corridor. China holds the largest national market share within the region, driven by its vast domestic construction and infrastructure programs, and is home to globally significant excavator manufacturers including SANY Group and XCMG Group, whose cost-competitive machines have expanded rapidly beyond China into developing market export opportunities. India is the fastest-growing individual national market within Asia-Pacific, propelled by its urbanization trajectory, national highway and railway investment programs, and the institutional framework established by NaBFID for long-term infrastructure financing.

North America holds the second-largest market and is expected to grow at a strong CAGR through the forecast period, fueled by the Infrastructure Investment and Jobs Act’s multi-year construction spending commitments across roads, bridges, rail, broadband, water systems, and clean energy infrastructure. The US dominates regional demand, with Canada’s resource sector and construction activity providing supplementary volume. Caterpillar, John Deere, and Volvo Construction Equipment’s North American manufacturing and distribution networks anchor the competitive landscape, while SANY and XCMG’s growing US dealer networks reflect Chinese manufacturers’ strategic push into the world’s most valuable excavator market.

Europe holds the second-largest share globally, characterized by mature markets with high technical specifications, stringent emission standards that are driving accelerated transition to Stage V compliant and electric machines, and significant infrastructure renewal investment programs. Germany, France, the UK, and Italy are the leading national markets, with Volvo CE, JCB, Doosan Infracore, and Kobelco among the prominent European and European-market-focused producers.

Rest of World — encompassing the Middle East, Africa, and Latin America — represents the most dynamic emerging growth frontier, with Middle Eastern megaprojects (NEOM and GCC infrastructure programs), African mining expansion, and Latin American infrastructure and resource sector investment all generating growing excavator demand that is attracting dedicated model development and distribution investment from global OEMs.

Competitive Landscape and Key Industry Developments

The global excavator industry is moderately concentrated at the top, with Caterpillar (US), Komatsu (Japan), Hitachi Construction Machinery (Japan), Volvo Construction Equipment (Sweden), SANY Group (China), XCMG Group (China), John Deere (US), JCB (UK), Doosan Infracore (South Korea), and Kobelco Construction Machinery (Japan) collectively commanding the majority of global market revenue. The competitive dynamic is defined by a tension between the established Japanese, American, and European OEMs with strong technology, brand, and service network advantages, and the Chinese manufacturers’ rapidly improving quality, cost-competitiveness, and aggressive international expansion.

Caterpillar’s AI-driven excavator development partnership signals its intent to maintain technology leadership as intelligence becomes a primary differentiator. Komatsu’s hybrid excavator line launch and digital construction platform positioning reflect Japan’s industry tradition of leading the hybridization and automation of heavy equipment. Volvo CE’s electric excavator product development and 2030 carbon neutrality commitment exemplify the European industry’s regulatory-driven sustainability leadership. Caterpillar’s January 2024 introduction of its 336 Next Generation excavator — featuring Tier 4 Final compliance, redesigned cab, and productivity-enhancing technologies — demonstrates the continuous improvement philosophy that sustains incumbent OEMs’ performance leadership. Tata Hitachi’s NX30 Mini Excavator — designed in India for Indian market conditions and manufactured locally under the Atmanirbhar mission — exemplifies the localization strategy that global and regional OEMs are deploying to serve the specific performance, maintenance, and cost requirements of high-growth developing markets.

Future Outlook and Conclusion

The global Excavators Market is advancing with confidence toward USD 134.3 billion by 2035, at a 5.50% CAGR sustained by the world’s most fundamental infrastructure needs: moving earth to create the roads, buildings, mines, pipelines, and utilities upon which civilization depends. The decade ahead will be defined by three simultaneous transformations: the electrification of the compact and mini excavator fleet as battery technology matures and urban zero-emission zone regulations spread; the intelligent automation of excavators through AI, machine control, and telematics integration that is transforming operators from machine controllers into productivity managers; and the expanding application of excavators in the mining sectors serving the critical minerals demands of global electrification. New strategic opportunities are crystallizing in the development of electric and hydrogen-powered excavator platforms for emission-restricted markets, the integration of IoT and fleet intelligence for real-time productivity and maintenance optimization, and the expansion into emerging markets through localized manufacturing, specialized financing solutions, and tailored product configurations that serve the specific conditions of rapidly growing construction economies. For manufacturers, rental operators, contractors, infrastructure developers, mining companies, and investors in construction and industrial equipment, the excavator market’s combination of structural demand depth, technological dynamism, and geographic growth breadth makes it one of the most compelling investment and commercial opportunity landscapes in global industrial equipment for the decade ahead.

For more insights on Market, visit the Market Research Future page and explore detailed market analysis, forecasts, and company strategies.

Security Label Market

Soft Drinks Packaging Market

Food Container Market

Industrial Packaging Market

Meat, Poultry, Seafood Packaging Market

Airless Packaging Market

Bulk Bags Market